Credit Card Fraud Detection with Logistic Regression

Intro

We will build a logistic regression model using PCA transformed data. Dataset: data/creditcard.csv source: Kaggle

The assumption of this model is that both of normal and fraud transactions can be separated by a single linear boundary. Also, I assumed the fraud techniques stay same, i.e. this model is valid over long term (otherwise, this model becomes useless other than self practice purpose).

Import packages

from freq_utils import fsize, plot_learning_curve # freq_utils.py is my custom file

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import train_test_split

from sklearn.metrics import confusion_matrix

from sklearn.metrics import accuracy_score, precision_score, recall_score, f1_score

from sklearn.metrics import roc_curve, auc, log_loss

from sklearn.metrics import make_scorer

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import ShuffleSplit

from sklearn.model_selection import GridSearchCV

# figure cosmetic function

def fsize(w,h,c=False):

# set figure size

plt.rcParams["figure.figsize"] = [w, h]

# adjust plot automatically

plt.rcParams['figure.constrained_layout.use'] = c

Read dataset

df_read = pd.read_csv("data/creditcard.csv")

df_read.info()

print(df_read.duplicated().value_counts())

df_read.head()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 284807 entries, 0 to 284806

Data columns (total 31 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Time 284807 non-null float64

1 V1 284807 non-null float64

2 V2 284807 non-null float64

3 V3 284807 non-null float64

4 V4 284807 non-null float64

5 V5 284807 non-null float64

6 V6 284807 non-null float64

7 V7 284807 non-null float64

8 V8 284807 non-null float64

9 V9 284807 non-null float64

10 V10 284807 non-null float64

11 V11 284807 non-null float64

12 V12 284807 non-null float64

13 V13 284807 non-null float64

14 V14 284807 non-null float64

15 V15 284807 non-null float64

16 V16 284807 non-null float64

17 V17 284807 non-null float64

18 V18 284807 non-null float64

19 V19 284807 non-null float64

20 V20 284807 non-null float64

21 V21 284807 non-null float64

22 V22 284807 non-null float64

23 V23 284807 non-null float64

24 V24 284807 non-null float64

25 V25 284807 non-null float64

26 V26 284807 non-null float64

27 V27 284807 non-null float64

28 V28 284807 non-null float64

29 Amount 284807 non-null float64

30 Class 284807 non-null int64

dtypes: float64(30), int64(1)

memory usage: 67.4 MB

False 283726

True 1081

dtype: int64

| Time | V1 | V2 | V3 | V4 | V5 | V6 | V7 | V8 | V9 | ... | V21 | V22 | V23 | V24 | V25 | V26 | V27 | V28 | Amount | Class | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.0 | -1.359807 | -0.072781 | 2.536347 | 1.378155 | -0.338321 | 0.462388 | 0.239599 | 0.098698 | 0.363787 | ... | -0.018307 | 0.277838 | -0.110474 | 0.066928 | 0.128539 | -0.189115 | 0.133558 | -0.021053 | 149.62 | 0 |

| 1 | 0.0 | 1.191857 | 0.266151 | 0.166480 | 0.448154 | 0.060018 | -0.082361 | -0.078803 | 0.085102 | -0.255425 | ... | -0.225775 | -0.638672 | 0.101288 | -0.339846 | 0.167170 | 0.125895 | -0.008983 | 0.014724 | 2.69 | 0 |

| 2 | 1.0 | -1.358354 | -1.340163 | 1.773209 | 0.379780 | -0.503198 | 1.800499 | 0.791461 | 0.247676 | -1.514654 | ... | 0.247998 | 0.771679 | 0.909412 | -0.689281 | -0.327642 | -0.139097 | -0.055353 | -0.059752 | 378.66 | 0 |

| 3 | 1.0 | -0.966272 | -0.185226 | 1.792993 | -0.863291 | -0.010309 | 1.247203 | 0.237609 | 0.377436 | -1.387024 | ... | -0.108300 | 0.005274 | -0.190321 | -1.175575 | 0.647376 | -0.221929 | 0.062723 | 0.061458 | 123.50 | 0 |

| 4 | 2.0 | -1.158233 | 0.877737 | 1.548718 | 0.403034 | -0.407193 | 0.095921 | 0.592941 | -0.270533 | 0.817739 | ... | -0.009431 | 0.798278 | -0.137458 | 0.141267 | -0.206010 | 0.502292 | 0.219422 | 0.215153 | 69.99 | 0 |

5 rows × 31 columns

Data formats are valid. No empty record but duplication.

# drop duplication

df_read.drop_duplicates(inplace=True)

# Check number of each class

df_read.Class.value_counts()

0 283253

1 473

Name: Class, dtype: int64

Undersampling and Train Test Split

To fit logistic regression, class should be sampled in valance. I’ll balance the number of samples by undersampling since we have enough data.

Then split train and test sets before explore data.

# Split datasets separatively for each class

normal = df_read[df_read.Class==0]

fraud = df_read[df_read.Class==1]

normal0, normal2 = train_test_split(normal, test_size = 0.2, random_state=1)

normal0, normal1 = train_test_split(normal0, test_size = 0.2, random_state=2)

fraud0, fraud2 = train_test_split(fraud, test_size = 0.2, random_state=3)

fraud0, fraud1 = train_test_split(fraud0, test_size = 0.2, random_state=4)

# Undersampling for training and dev sets

df = pd.concat([fraud0,normal0.sample(len(fraud0))])

df_dev = pd.concat([fraud1,normal1.sample(len(fraud1))])

# Make a test sample realistic, i.e. 0.172% of transactions are fraud

df_test = pd.concat([fraud2, normal2])

EDA and Feature Engineering

Time and amount

Before begin, let’s check features we know.

fsize(16,8)

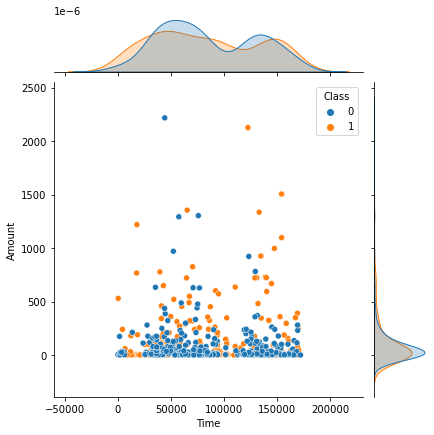

# Time and Amount joint plot with Class hue

sns.jointplot(x='Time', y='Amount', data=df, hue='Class',)

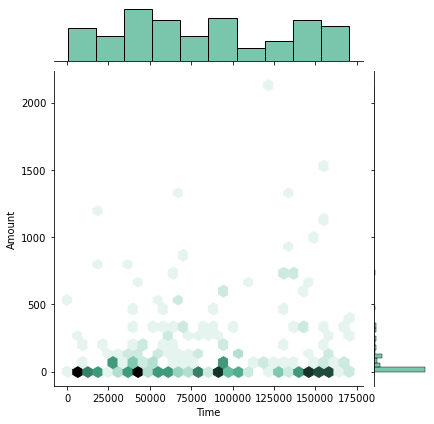

sns.jointplot(x='Time', y='Amount', data=df[df.Class==1], kind="hex", color="#4CB391")

<seaborn.axisgrid.JointGrid at 0x7fea873cf760>

No noticable item to separate two classes only with Amount or Time. Unlike my expectation, the typical amount of fraud is very little.

Select features

We will select features which have high correlation with Class. While selecting features, other features with too high correlation with the selected feature will be dropped.

# sort features according to correlation with class

sorted_features = df.corr().Class.abs().sort_values(ascending=False).drop('Class').index.to_numpy()

# features to drop

to_drop = set()

# add features to drop due to high correlation with another

for x in sorted_features:

if x in to_drop:

continue

for y in sorted_features:

if y in to_drop:

continue

elif x==y:

continue

else:

val = df[x].corr(df[y])

if val>0.85:

to_drop.add(y)

print('Features to drop:',to_drop)

Features to drop: {'V12', 'V7', 'V16', 'V18', 'V3'}

# Select highly correlated features again

sorted_features = df.corr().Class.abs().sort_values(ascending=False).drop('Class').drop(list(to_drop))

print('Feature correlation with Class:\n', sorted_features)

Feature correlation with Class:

V14 0.720942

V4 0.694075

V11 0.646819

V10 0.605722

V9 0.522540

V17 0.516138

V2 0.461733

V6 0.428790

V1 0.404820

V5 0.322045

V19 0.248267

V20 0.219867

V27 0.106493

V22 0.105856

V15 0.090137

V28 0.087062

V24 0.086127

Amount 0.085669

V21 0.079010

V8 0.073927

V23 0.065870

V13 0.038041

V25 0.031948

V26 0.028809

Time 0.026600

Name: Class, dtype: float64

# Dataframe for train and test

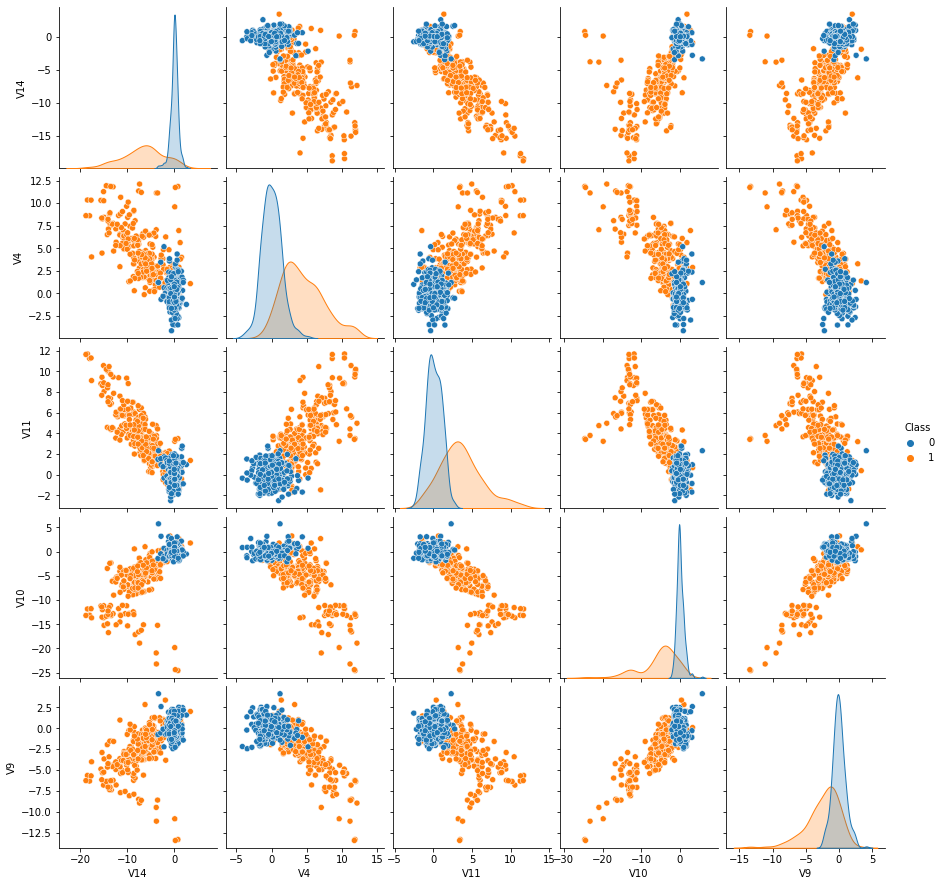

# Select 5 features for now, to check distribution

selected_features = sorted_features.iloc[:5]

train = df[selected_features.index.tolist()+['Class']]

# Visualize correlations and distributions

sns.pairplot(train, hue="Class")

plt.show()

- From this pair plot, we can see that those selected features have high classification power.

- Also, each feature separates two classes with a single straight boundary. Logistic regression will perform well here.

- I noticed that the features are not scaled. Let’s do it.

Feature scaling

scaler = StandardScaler()

# fit with training set

scaler.fit(df.drop('Class',axis=1))

# transform all sets

df[df.columns[:-1]] = scaler.transform(df.drop('Class',axis=1))

df_dev[df_dev.columns[:-1]] = scaler.transform(df_dev.drop('Class',axis=1))

df_test[df_test.columns[:-1]] = scaler.transform(df_test.drop('Class',axis=1))

# Confirm transformation result

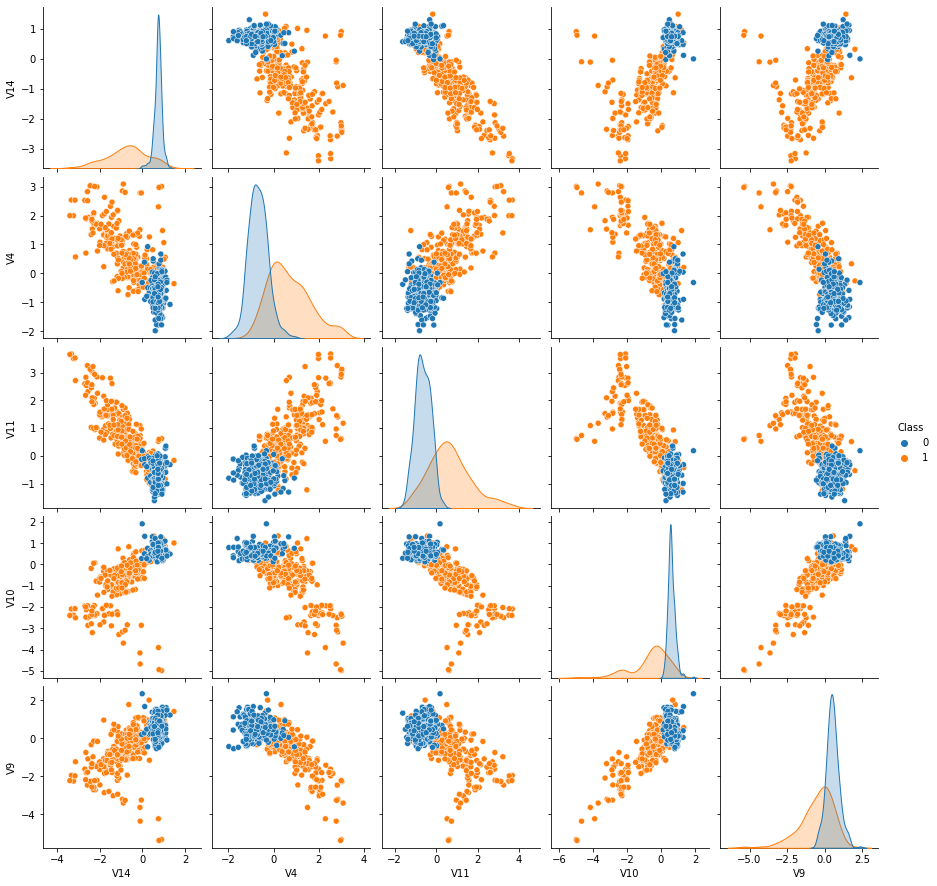

train = df[selected_features.index.tolist()+['Class']]

sns.pairplot(train, hue="Class")

plt.show()

Train

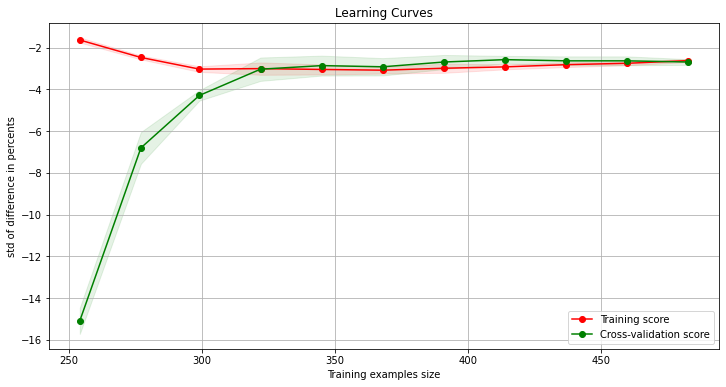

Let’s train and plot learning curve. For the cost function, I’ll use cross entropy.

def learning_curve_wrapper(X,y):

n_samples = X.shape[0]

cv = ShuffleSplit(n_splits=10, test_size=0.3, random_state=0)

model = LogisticRegression()

#scorer = make_scorer(recall_score, greater_is_better=True)

scorer = make_scorer(log_loss, greater_is_better=False)

title = "Learning Curves"

plot_learning_curve(model, title, X, y, scoring=scorer, train_sizes=np.linspace(.1, 1.0, 20))

plt.show()

return model

fsize(12,6)

model = learning_curve_wrapper(train[train.columns[:-1]], train.Class)

Both of training and validation scores saturated at the similar score. No sign of overfit.

Hypermarameter tuning

Hyper parameters can be

- Number of selected features

- Regularization parameters.

Here, I’ll try with l1 and l2 regularization with “liblinear” obtimization algorithm because it is a good choice for small dataset.

# loop over scoring metric

model_var = []

imodel = 0

#for scoring in ['recall','accuracy','precision', 'f1']:

# loop over number of features

for num_features in range(1,20):

selected_features = sorted_features.iloc[:num_features]

train = df[selected_features.index.tolist()+['Class']]

dev = df_dev[selected_features.index.tolist()+['Class']]

X_train = train[train.columns[:-1]]

y_train = train.Class

X_dev = dev[dev.columns[:-1]]

y_dev = dev.Class

# logistic regression with L2 regularization

# obtimization is liblinear

model = LogisticRegression(solver='liblinear')

penalty= ['l1','l2']

# inverse of regularization strength

# smaller values specify stronger regularization

C = [100, 30, 10, 3.0, 1.0, 0.3, 0.1, 0.03, 0.01]

# dictionary of hyperparameters

distributions = dict(penalty=penalty, C=C)

# grid search

clf = GridSearchCV(model, distributions, scoring='neg_log_loss', cv=5)

search = clf.fit(X_train, y_train)

# best hyperparameter dict

bp = search.best_params_

# test score with vaildation set

model = LogisticRegression(solver='liblinear', penalty=bp['penalty'], C=bp['C'])

model.fit(X_train, y_train)

y_pred = model.predict(X_dev)

y_proba = model.predict_proba(X_dev)

y_proba = y_proba[:,1]

rc = recall_score(y_dev,y_pred)

ac = accuracy_score(y_dev,y_pred)

pr = precision_score(y_dev,y_pred)

f1 = f1_score(y_dev,y_pred)

coefs = pd.Series(model.coef_.flatten(), index = selected_features.index.tolist())

model_var.append([imodel,model,coefs,num_features])#, y_pred,y_proba])

print(imodel, num_features, bp, '\t', round(rc, 3),round(ac, 3),round(pr, 3),round(f1, 3) )

imodel+=1

0 1 {'C': 30, 'penalty': 'l2'} 0.947 0.961 0.973 0.96

1 2 {'C': 10, 'penalty': 'l2'} 0.934 0.934 0.934 0.934

2 3 {'C': 3.0, 'penalty': 'l2'} 0.934 0.941 0.947 0.94

3 4 {'C': 3.0, 'penalty': 'l2'} 0.934 0.947 0.959 0.947

4 5 {'C': 3.0, 'penalty': 'l2'} 0.947 0.954 0.96 0.954

5 6 {'C': 3.0, 'penalty': 'l2'} 0.934 0.947 0.959 0.947

6 7 {'C': 3.0, 'penalty': 'l2'} 0.934 0.954 0.973 0.953

7 8 {'C': 3.0, 'penalty': 'l2'} 0.947 0.954 0.96 0.954

8 9 {'C': 3.0, 'penalty': 'l2'} 0.947 0.961 0.973 0.96

9 10 {'C': 3.0, 'penalty': 'l2'} 0.947 0.961 0.973 0.96

10 11 {'C': 3.0, 'penalty': 'l2'} 0.947 0.961 0.973 0.96

11 12 {'C': 3.0, 'penalty': 'l2'} 0.947 0.961 0.973 0.96

12 13 {'C': 1.0, 'penalty': 'l1'} 0.947 0.961 0.973 0.96

13 14 {'C': 1.0, 'penalty': 'l1'} 0.947 0.954 0.96 0.954

14 15 {'C': 1.0, 'penalty': 'l1'} 0.947 0.954 0.96 0.954

15 16 {'C': 1.0, 'penalty': 'l1'} 0.947 0.947 0.947 0.947

16 17 {'C': 1.0, 'penalty': 'l1'} 0.947 0.947 0.947 0.947

17 18 {'C': 1.0, 'penalty': 'l2'} 0.947 0.961 0.973 0.96

18 19 {'C': 1.0, 'penalty': 'l2'} 0.934 0.954 0.973 0.953

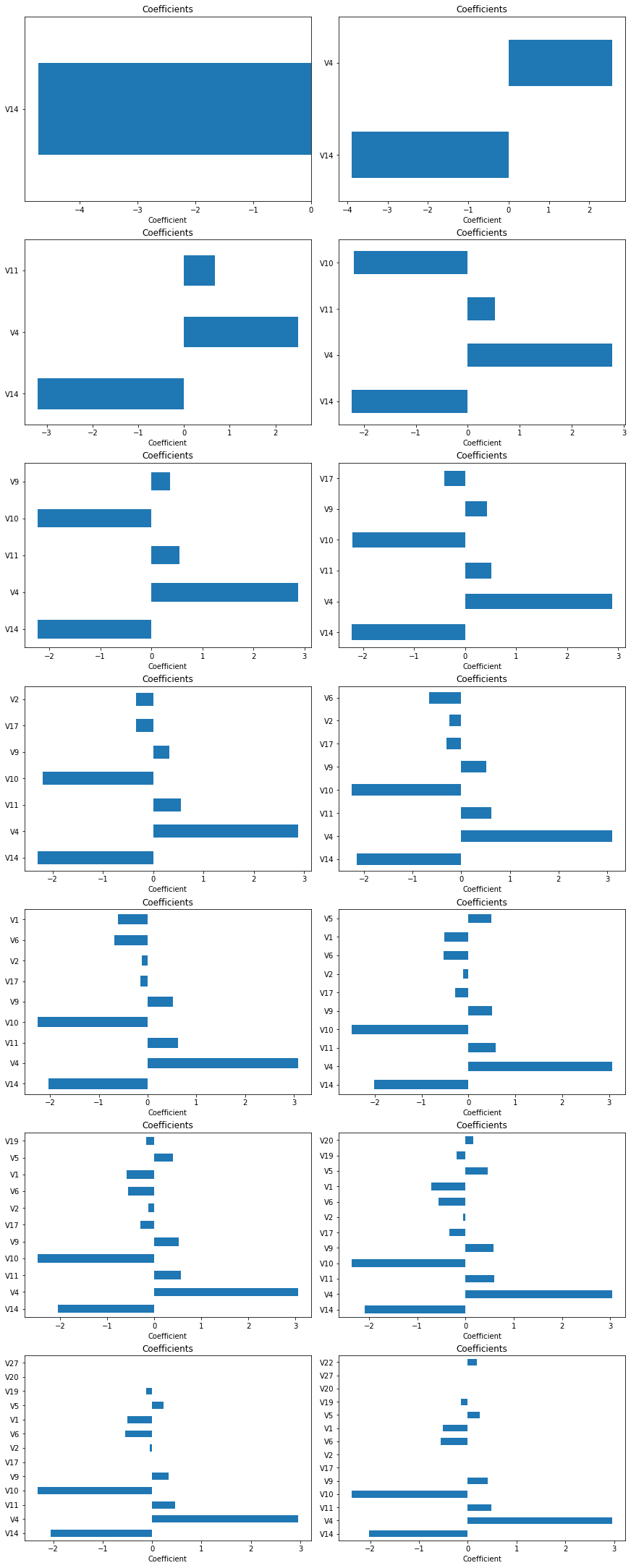

Overall, performances are similar. Best Model 5 has slightly better performance, but it changes whenever I run the code (I don’t know if I can fix random state of GridSearchCV). For closer look, let’s plot feature coefficient together for first few cases.

# Plot features with high coefficient (leading features)

fsize(12,30,True)

for i in range(0,14):

plt.subplot(7,2,i+1)

_, model, coefs, num_features = model_var[i]

#coefs = pd.concat([coefs.sort_values().head(7),

# coefs.sort_values().tail(8)])

coefs.plot.barh()

plt.xlabel('Coefficient')

ax = plt.title("Coefficients")

While coefficients of the first four leading components look quite consistent, 5th component was not stable. Also, V1 and V5 components seem to contribute quite a lot consistently. Let’s try include them along with the first four component, and see if it improves this model.

train = df[['V14','V4','V11','V10','V1','V5','Class']]

dev = df_dev[['V14','V4','V11','V10','V1','V5','Class']]

X_train = train[train.columns[:-1]]

y_train = train.Class

X_dev = dev[dev.columns[:-1]]

y_dev = dev.Class

# logistic regression with L2 regularization

# obtimization is liblinear

model = LogisticRegression(solver='liblinear')

penalty= ['l1','l2']

# inverse of regularization strength

# smaller values specify stronger regularization

C = [100, 30, 10, 3.0, 1.0, 0.3, 0.1, 0.03, 0.01]

# dictionary of hyperparameters

distributions = dict(penalty=penalty, C=C)

# grid search

clf = GridSearchCV(model, distributions, scoring='neg_log_loss', cv=5)

search = clf.fit(X_train, y_train)

# best hyperparameter dict

bp = search.best_params_

# test score with vaildation set

model = LogisticRegression(solver='liblinear', penalty=bp['penalty'], C=bp['C'])

model.fit(X_train, y_train)

y_pred = model.predict(X_dev)

y_proba = model.predict_proba(X_dev)

y_proba = y_proba[:,1]

rc = recall_score(y_dev,y_pred)

ac = accuracy_score(y_dev,y_pred)

pr = precision_score(y_dev,y_pred)

f1 = f1_score(y_dev,y_pred)

coefs = pd.Series(model.coef_.flatten(), index = ['V14','V4','V11','V10','V1','V5'])

print(bp, '\t', round(rc, 3),round(ac, 3),round(pr, 3),round(f1, 3) )

{'C': 3.0, 'penalty': 'l2'} 0.934 0.947 0.959 0.947

No, it didn’t improve.

So, for our final model, let’s include only the first 4 components, which were leading components consistently. This model number is 3.

Test and Results

# get a final model

_, model, coefs, num_features = model_var[3]

selected_features = sorted_features.iloc[:num_features]

X_test = df[selected_features.index]

y_test = df.Class

# get prediction

y_pred = model.predict(X_test)

y_proba = model.predict_proba(X_test)

y_proba = y_proba[:,1]

# print scores

rc = recall_score(y_test,y_pred)

ac = accuracy_score(y_test,y_pred)

pr = precision_score(y_test,y_pred)

f1 = f1_score(y_test,y_pred)

print('Scores:',round(rc, 3),round(ac, 3),round(pr, 3),round(f1, 3) )

print(selected_features, model.coef_, model.intercept_)

print(confusion_matrix(y_test, y_pred))

Scores: 0.871 0.925 0.978 0.921

V14 0.720942

V4 0.694075

V11 0.646819

V10 0.605722

Name: Class, dtype: float64 [[-2.23133532 2.77847589 0.519276 -2.19161554]] [2.68467681]

[[296 6]

[ 39 263]]

V14, V4, and V10 played the most significant contribution. This model gave high recall score, 0.90, while giving very high precision, 0.98.

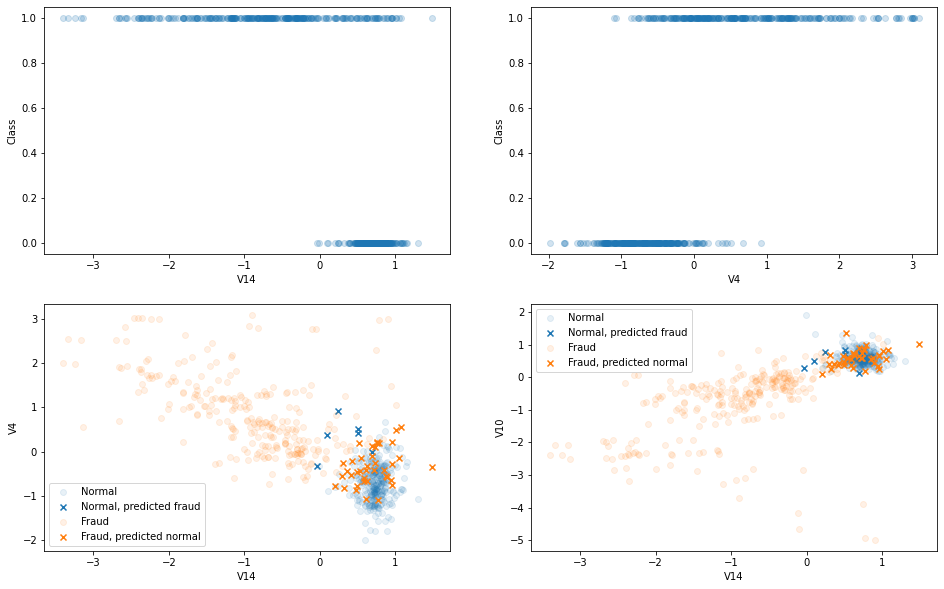

fsize(16,10)

test = X_test.copy()

test['Class'] = y_test

plt.subplot(2,2,1)

plt.scatter(X_test.V14, y_test, alpha=0.2)

plt.xlabel('V14')

plt.ylabel('Class')

plt.subplot(2,2,2)

plt.scatter(X_test.V4, y_test, alpha=0.2)

plt.xlabel('V4')

plt.ylabel('Class')

plt.subplot(2,2,3)

test['pred']= y_pred

X = test[(test.Class==0)&(test.pred==0)]

plt.scatter(X.V14, X.V4, color='tab:blue', alpha=0.1, label='Normal')

X = test[(test.Class==0)&(test.pred==1)]

plt.scatter(X.V14, X.V4, color='tab:blue', marker='x', label='Normal, predicted fraud')

X = test[(test.Class==1)&(test.pred==1)]

plt.scatter(X.V14, X.V4, color='tab:orange', alpha=0.1, label='Fraud')

X = test[(test.Class==1)&(test.pred==0)]

plt.scatter(X.V14, X.V4, color='tab:orange', marker='x', label='Fraud, predicted normal')

plt.xlabel('V14')

plt.ylabel('V4')

plt.legend()

plt.subplot(2,2,4)

X = test[(test.Class==0)&(test.pred==0)]

plt.scatter(X.V14, X.V10, color='tab:blue', alpha=0.1, label='Normal')

X = test[(test.Class==0)&(test.pred==1)]

plt.scatter(X.V14, X.V10, color='tab:blue', marker='x', label='Normal, predicted fraud')

X = test[(test.Class==1)&(test.pred==1)]

plt.scatter(X.V14, X.V10, color='tab:orange', alpha=0.1, label='Fraud')

X = test[(test.Class==1)&(test.pred==0)]

plt.scatter(X.V14, X.V10, color='tab:orange', marker='x', label='Fraud, predicted normal')

plt.xlabel('V14')

plt.ylabel('V10')

plt.legend()

<matplotlib.legend.Legend at 0x7fea801a6fa0>

Those plots visualize class overlapping regions.

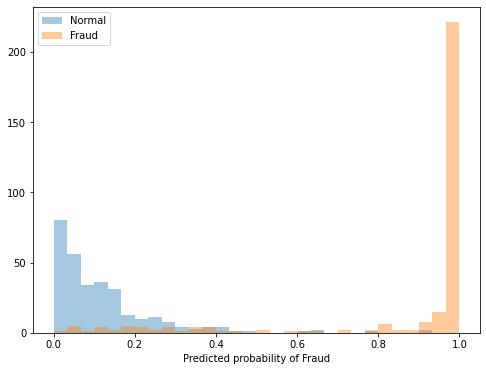

# plot probabilities

fsize(8,6)

X = test[test.Class==0].drop(['Class','pred'],axis=1)

ax =plt.hist(model.predict_proba(X)[:,1], bins=30, range=(0,1), label='Normal', alpha=0.4)

X = test[test.Class==1].drop(['Class','pred'],axis=1)

ax = plt.hist(model.predict_proba(X)[:,1], bins=30, range=(0,1), label='Fraud', alpha=0.4)

plt.xlabel('Predicted probability of Fraud')

plt.legend()

<matplotlib.legend.Legend at 0x7fea80239bb0>

While fraud events have a peak at predicted probability around 1, the predicted probability of normal transactions is more even out. This model is more strict for fraud.

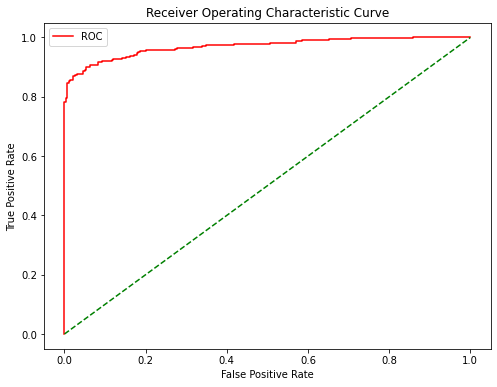

# Plot ROC curve

fsize(8,6)

fpr, tpr, thr = roc_curve(y_test, y_proba)

plt.plot(fpr, tpr, color='red', label='ROC')

plt.plot([0, 1], [0, 1], color='green', linestyle='--')

plt.xlabel('False Positive Rate')

plt.ylabel('True Positive Rate')

plt.title('Receiver Operating Characteristic Curve')

plt.legend()

plt.show()

Around TPR=0.8, false alarm rate start to increase rapidly. We might invent a two steps detection system, such as record anything over threshold of TPR=0.8, then immediately stop transaction following a model optimized for the high precision.

Leave a comment