Credit Card Fraud Detection with K-Nearest Neighbors

Intro

We will build a logistic regression model using PCA transformed data. Dataset: data/creditcard.csv source: Kaggle Previously, I built this model with Logistig regression. Let’t compare performance with kNN.

Here, I’ll skip EDA and use the same feature engineering as I’d done for Logistic regressions.

Import packages

from freq_utils import fsize # freq_utils.py is my custom file

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from sklearn.neighbors import KNeighborsClassifier

from sklearn.model_selection import train_test_split

from sklearn.metrics import confusion_matrix

from sklearn.metrics import accuracy_score, precision_score, recall_score, f1_score, roc_auc_score

from sklearn.preprocessing import StandardScaler

Read dataset

df_read = pd.read_csv("data/creditcard.csv")

# drop duplication

df_read.drop_duplicates(inplace=True)

Undersampling and Train Test Split

To make kNN works fairly, class should be sampled in valance. I’ll balance the number of samples by undersampling since we have enough data.

Then split train and test sets.

# Split datasets separatively for each class

normal = df_read[df_read.Class==0]

fraud = df_read[df_read.Class==1]

# In kNN, there's no model building thing. I think important thing is to determine proper k using dev set.

# To have good amount of data to determin k using dev set, I'll give more data to dev set than usual.

normal0, normal2 = train_test_split(normal, test_size = 0.2, random_state=1)

normal0, normal1 = train_test_split(normal0, test_size = 0.5, random_state=2)

fraud0, fraud2 = train_test_split(fraud, test_size = 0.2, random_state=3)

fraud0, fraud1 = train_test_split(fraud0, test_size = 0.5, random_state=4)

# Undersampling for training and dev sets

df = pd.concat([fraud0,normal0.sample(len(fraud0))])

df_dev = pd.concat([fraud1,normal1.sample(len(fraud1))])

# Make a test sample realistic, i.e. 0.172% of transactions are fraud

df_test = pd.concat([fraud2, normal2])

Feature engineering

Feature scaling

scaler = StandardScaler()

# fit with training set

scaler.fit(df.drop('Class',axis=1))

# transform all sets

df[df.columns[:-1]] = scaler.transform(df.drop('Class',axis=1))

df_dev[df_dev.columns[:-1]] = scaler.transform(df_dev.drop('Class',axis=1))

df_test[df_test.columns[:-1]] = scaler.transform(df_test.drop('Class',axis=1))

Feature selection

See logistic regression.

selected_features = ['V14','V4','V11','V10'] # determined from logistic regression project

X_train = df[selected_features]

X_dev = df_dev[selected_features]

X_test = df_test[selected_features]

y_train = df.Class

y_dev = df_dev.Class

y_test = df_test.Class

Hyperparameter tuning

Nothing special for training. It is simple. Let’s jump to hyperparameter tuning.

# list to save scores of each k

scores = []

for k in range(1,100): # I should find how the KNeighborsClassifier solves tie for even k

# pass training data info

model = KNeighborsClassifier(n_neighbors = k)

model.fit(X_train, y_train)

# get prediction of dev set

y_pred = model.predict(X_dev)

# print scores

rc = recall_score(y_dev,y_pred)

ac = accuracy_score(y_dev,y_pred)

pr = precision_score(y_dev,y_pred)

f1 = f1_score(y_dev,y_pred)

ra = roc_auc_score(y_dev,y_pred)

# append scores

scores.append([k, rc,ac,pr,f1,ra, model])

print('k=',k, '\t', round(rc, 3),round(ac, 3),round(pr, 3),round(f1, 3),round(ra, 3) )

k= 1 0.905 0.899 0.895 0.9 0.899

k= 2 0.878 0.923 0.965 0.92 0.923

k= 3 0.926 0.939 0.951 0.938 0.939

k= 4 0.894 0.944 0.994 0.942 0.944

k= 5 0.905 0.939 0.972 0.937 0.939

k= 6 0.878 0.934 0.988 0.93 0.934

k= 7 0.894 0.929 0.96 0.926 0.929

k= 8 0.878 0.934 0.988 0.93 0.934

k= 9 0.894 0.934 0.971 0.931 0.934

k= 10 0.889 0.934 0.977 0.931 0.934

k= 11 0.889 0.926 0.96 0.923 0.926

k= 12 0.884 0.931 0.977 0.928 0.931

k= 13 0.889 0.929 0.966 0.926 0.929

k= 14 0.889 0.931 0.971 0.928 0.931

k= 15 0.894 0.931 0.966 0.929 0.931

k= 16 0.884 0.931 0.977 0.928 0.931

k= 17 0.884 0.923 0.96 0.92 0.923

k= 18 0.884 0.926 0.965 0.923 0.926

k= 19 0.884 0.923 0.96 0.92 0.923

k= 20 0.884 0.931 0.977 0.928 0.931

k= 21 0.884 0.931 0.977 0.928 0.931

k= 22 0.884 0.934 0.982 0.93 0.934

k= 23 0.884 0.931 0.977 0.928 0.931

k= 24 0.884 0.937 0.988 0.933 0.937

k= 25 0.884 0.937 0.988 0.933 0.937

k= 26 0.878 0.934 0.988 0.93 0.934

k= 27 0.884 0.937 0.988 0.933 0.937

k= 28 0.884 0.937 0.988 0.933 0.937

k= 29 0.884 0.937 0.988 0.933 0.937

k= 30 0.878 0.934 0.988 0.93 0.934

k= 31 0.884 0.937 0.988 0.933 0.937

k= 32 0.878 0.937 0.994 0.933 0.937

k= 33 0.884 0.937 0.988 0.933 0.937

k= 34 0.884 0.939 0.994 0.936 0.939

k= 35 0.884 0.939 0.994 0.936 0.939

k= 36 0.878 0.937 0.994 0.933 0.937

k= 37 0.878 0.937 0.994 0.933 0.937

k= 38 0.878 0.937 0.994 0.933 0.937

k= 39 0.878 0.937 0.994 0.933 0.937

k= 40 0.878 0.937 0.994 0.933 0.937

k= 41 0.878 0.937 0.994 0.933 0.937

k= 42 0.878 0.937 0.994 0.933 0.937

k= 43 0.878 0.937 0.994 0.933 0.937

k= 44 0.878 0.939 1.0 0.935 0.939

k= 45 0.878 0.939 1.0 0.935 0.939

k= 46 0.878 0.939 1.0 0.935 0.939

k= 47 0.878 0.939 1.0 0.935 0.939

k= 48 0.873 0.937 1.0 0.932 0.937

k= 49 0.878 0.939 1.0 0.935 0.939

k= 50 0.873 0.937 1.0 0.932 0.937

k= 51 0.873 0.937 1.0 0.932 0.937

k= 52 0.873 0.937 1.0 0.932 0.937

k= 53 0.873 0.937 1.0 0.932 0.937

k= 54 0.873 0.937 1.0 0.932 0.937

k= 55 0.873 0.937 1.0 0.932 0.937

k= 56 0.873 0.937 1.0 0.932 0.937

k= 57 0.873 0.937 1.0 0.932 0.937

k= 58 0.873 0.937 1.0 0.932 0.937

k= 59 0.873 0.937 1.0 0.932 0.937

k= 60 0.868 0.934 1.0 0.929 0.934

k= 61 0.868 0.934 1.0 0.929 0.934

k= 62 0.868 0.934 1.0 0.929 0.934

k= 63 0.868 0.934 1.0 0.929 0.934

k= 64 0.868 0.934 1.0 0.929 0.934

k= 65 0.868 0.934 1.0 0.929 0.934

k= 66 0.868 0.934 1.0 0.929 0.934

k= 67 0.868 0.934 1.0 0.929 0.934

k= 68 0.868 0.934 1.0 0.929 0.934

k= 69 0.868 0.934 1.0 0.929 0.934

k= 70 0.868 0.934 1.0 0.929 0.934

k= 71 0.868 0.934 1.0 0.929 0.934

k= 72 0.868 0.934 1.0 0.929 0.934

k= 73 0.868 0.934 1.0 0.929 0.934

k= 74 0.868 0.934 1.0 0.929 0.934

k= 75 0.868 0.934 1.0 0.929 0.934

k= 76 0.868 0.934 1.0 0.929 0.934

k= 77 0.868 0.934 1.0 0.929 0.934

k= 78 0.868 0.934 1.0 0.929 0.934

k= 79 0.868 0.934 1.0 0.929 0.934

k= 80 0.868 0.934 1.0 0.929 0.934

k= 81 0.868 0.934 1.0 0.929 0.934

k= 82 0.868 0.934 1.0 0.929 0.934

k= 83 0.868 0.934 1.0 0.929 0.934

k= 84 0.868 0.934 1.0 0.929 0.934

k= 85 0.868 0.934 1.0 0.929 0.934

k= 86 0.868 0.934 1.0 0.929 0.934

k= 87 0.868 0.934 1.0 0.929 0.934

k= 88 0.868 0.934 1.0 0.929 0.934

k= 89 0.868 0.934 1.0 0.929 0.934

k= 90 0.868 0.934 1.0 0.929 0.934

k= 91 0.868 0.934 1.0 0.929 0.934

k= 92 0.868 0.934 1.0 0.929 0.934

k= 93 0.868 0.934 1.0 0.929 0.934

k= 94 0.868 0.934 1.0 0.929 0.934

k= 95 0.868 0.934 1.0 0.929 0.934

k= 96 0.868 0.934 1.0 0.929 0.934

k= 97 0.868 0.934 1.0 0.929 0.934

k= 98 0.868 0.934 1.0 0.929 0.934

k= 99 0.868 0.934 1.0 0.929 0.934

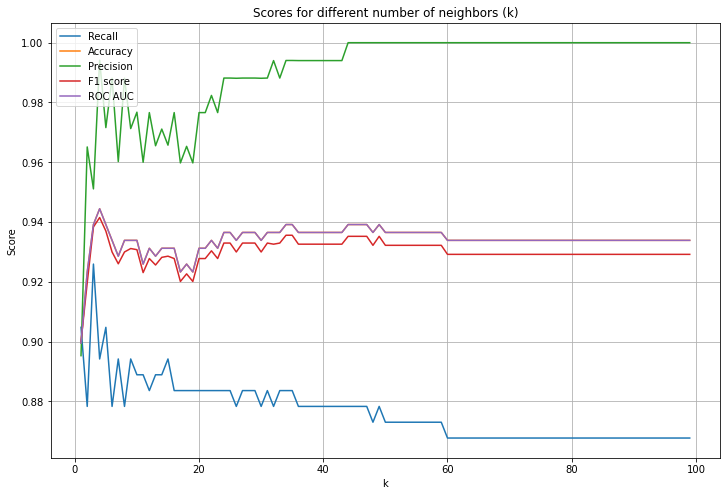

# Plot dev sert scores

fsize(12,8)

# reconstruct tuning parameters lists

k = [x[0] for x in scores]

rc = [x[1] for x in scores]

ac = [x[2] for x in scores]

pr = [x[3] for x in scores]

f1 = [x[4] for x in scores]

ra = [x[5] for x in scores]

# plot

plt.plot(k,rc,label='Recall')

plt.plot(k,ac,label='Accuracy')

plt.plot(k,pr,label='Precision')

plt.plot(k,f1,label='F1 score')

plt.plot(k,ra,label='ROC AUC')

plt.legend()

plt.xlabel('k')

plt.ylabel('Score')

plt.title('Scores for different number of neighbors (k)')

plt.grid()

I’ll choose k=27 because it gave relatively good recall, F1, AUC scores, while k itself is not too small, having potential to overfit.

Test and Results

# final model: k=9

model = scores[9][6]

# get prediction of test set

y_pred = model.predict(X_test)

# print scores

print('Accuracy:',accuracy_score(y_test, y_pred))

print('Precision:',precision_score(y_test, y_pred))

print('Recall:',recall_score(y_test, y_pred))

print('F1:',f1_score(y_test, y_pred))

print('ROC AUC:',roc_auc_score(y_test, y_pred))

Accuracy: 0.9814612483699292

Precision: 0.07390917186108638

Recall: 0.8736842105263158

F1: 0.13628899835796388

ROC AUC: 0.9276630969490945

Recall is great, but precision is terrible. High accuracy is meaningless because of highly imbalanced dataset. The result is worse than the logistic regression model we built previously.

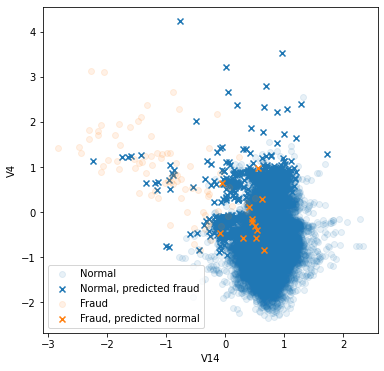

# plot distributions for leading two features

fsize(6,6)

test = X_test.copy()

test['pred']= y_pred

test['Class'] = y_test

X = test[(test.Class==0)&(test.pred==0)]

plt.scatter(X.V14, X.V4, color='tab:blue', alpha=0.1, label='Normal')

X = test[(test.Class==0)&(test.pred==1)]

plt.scatter(X.V14, X.V4, color='tab:blue', marker='x', label='Normal, predicted fraud')

X = test[(test.Class==1)&(test.pred==1)]

plt.scatter(X.V14, X.V4, color='tab:orange', alpha=0.1, label='Fraud')

X = test[(test.Class==1)&(test.pred==0)]

plt.scatter(X.V14, X.V4, color='tab:orange', marker='x', label='Fraud, predicted normal')

plt.xlabel('V14')

plt.ylabel('V4')

plt.legend(loc=3)

<matplotlib.legend.Legend at 0x7fccd8f387f0>

We didn’t miss too much fraud transaction, as also seen from the high recall score. However, we marked too much of normal transaction as fraud. Compared to logistic regression, here’s what I guess.

- From the plot above, the normal events are spread over large area whereas fraud events are not. Fraud events have more density, so it has advantage to be selected as “the nearest neighbor”.

Conclusion - comparison to logistic regression

Overall, the performance of logistic regression was better than kNN in this project. I can list two main reasons which explain why.

- Fraud events are more dense in the n (number of used features) dimension space. That made kNN to select fraud events more in the thick gray area.

- Two classes are separated with a linear decision boundary. In this case, logistic regression works well.

Leave a comment