Credit Card Fraud Detection with Anomaly Detection

Intro

Goal

-

Detect most of fraudulent transaction without losing too much precision

-

Build a simple intuitive model in order to tune easily whenever fraudulent trend changes

Dataset

-

Provided by the Machine Learning Group of Université Libre de Bruxelles.

-

https://www.kaggle.com/mlg-ulb/creditcardfraud (144 MB, too large to upload to GitHub)

-

284,807 transactions, 492 of them (0.172%) are frauds.

-

30 numerical features: time, amount of meony, 28 PCA transformed components of encrypted data

Model

-

Supervised anomaly (outlier) detection based on Z-scores

-

Selected features having “high classification power”

-

Suggested best hyper parameters for two kind of “best choices”

Result

- Both models showed expected and excellent performance on the test set

Import modules and read dataset

import pandas as pd

import numpy as np

import seaborn as sns

import matplotlib.pyplot as plt

from sklearn.model_selection import train_test_split

#df = pd.read_csv('creditcard.csv') # original

df = pd.read_csv('creditcard_reduced.csv') # 50% random sample of original

Organize data

# df.duplicated() # -> no duplication

# df.info() # -> no NaN

# Features: ['Time', 'Amount', 'V1', 'V2', ... 'V28']

# Classification: 0 normal, 1 fraud

# split dataset to normal and fraud transaction

df0 = df.loc[df.Class==0].copy()

df1 = df.loc[df.Class==1].copy()

#df_write = pd.concat([df1.sample(n=246),df0.sample(n=142403)])

#df_write.to_csv('creditcard_reduced.csv', index=False)

Split dataset - Train/Cross validation/Test

df0_train, df0_test = train_test_split(df0, test_size=0.4)

df1_train, df1_test = train_test_split(df1, test_size=0.4)

df0_dev, df0_test = train_test_split(df0_test, test_size=0.5)

df1_dev, df1_test = train_test_split(df1_test, test_size=0.5)

Train - Z score parameter

features = df0_train.columns.drop(labels='Class')

df0_stat = df0_train[features].describe().T

# get Z-score parameter

mu0=df0_stat['mean']

sig0=df0_stat['std']

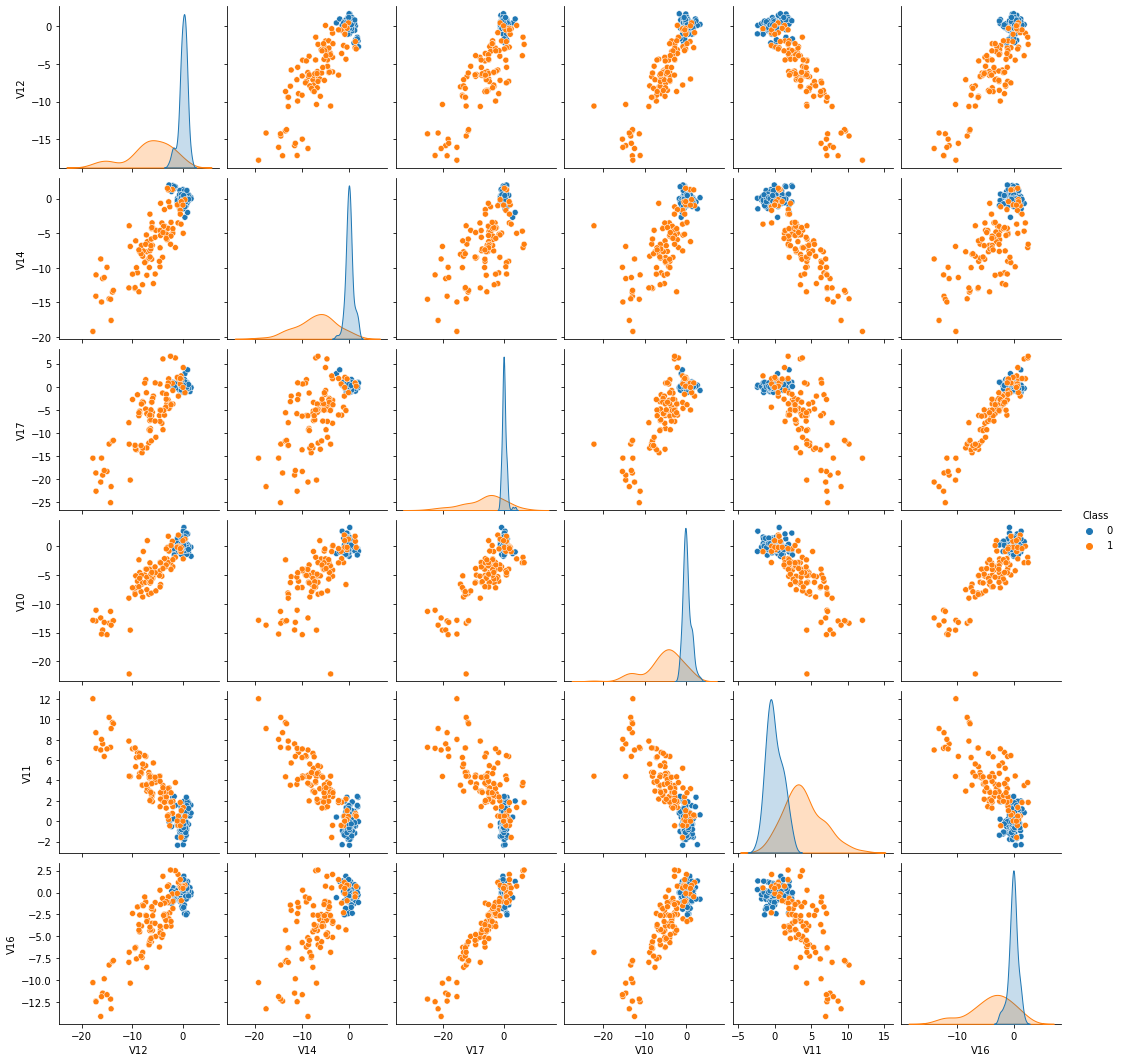

Visualize classsification power for selected features

# Recall of each features with two sized Z-score classification with two-sigma cut

dfz = ((abs(df1_train[features]-mu0[features])/sig0[features]) > 2).mean().sort_values(ascending=False)

sorted_feature = dfz.index.tolist()

feature_lead = sorted_feature[:6] ## leading classifying features

feature_insig = sorted_feature[-6:] ## not significantly classifying features

feature_lead.append('Class')

feature_insig.append('Class')

# Significantly classificatory features - high Z score

df_sig = pd.concat([df0_train[feature_lead].sample(n=100),df1_train[feature_lead].sample(n=100)])

sns.pairplot(df_sig, hue="Class")

plt.show()

Note: Keep in mind that the above plots are drawn for equal number of samples for both normal and fraud samples. With actual highly skewed samples, the distribution of normal sample will have much thicker tails.

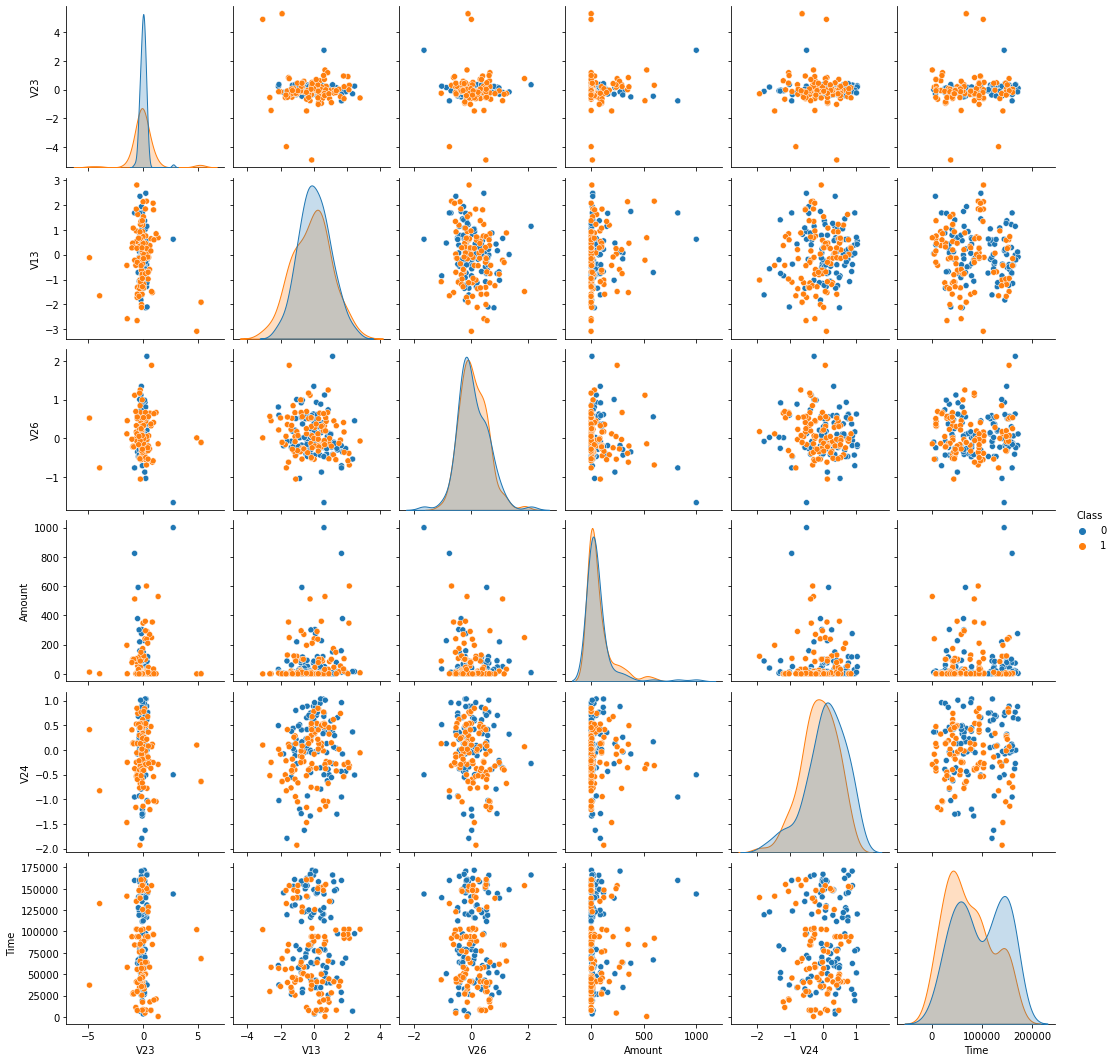

# Inignificantly classificatory features - low Z score

df_insig = pd.concat([df0_train[feature_insig].sample(n=100),df1_train[feature_insig].sample(n=100)])

sns.pairplot(df_insig, hue="Class")

plt.show()

Define anomaly metric and scoring

\[Z = \sqrt{\frac{1}{n}\sum^{n~\textrm{leading features}}_{i}~\frac{(Z_{i}-\mu_{i})^2}{\sigma_{i}^2} } > \epsilon\]# Z-score transform

X_train1 = (df1_train[features]-mu0[features])**2/sig0[features]**2

X_dev0 = (df0_dev[features]-mu0[features])**2/sig0[features]**2

X_dev1 = (df1_dev[features]-mu0[features])**2/sig0[features]**2

X_test0 = (df0_test[features]-mu0[features])**2/sig0[features]**2

X_test1 = (df1_test[features]-mu0[features])**2/sig0[features]**2

y_dev0 = df0_dev.Class

y_dev1 = df1_dev.Class

y_test0 = df0_test.Class

y_test1 = df1_test.Class

X_dev = pd.concat([X_dev0, X_dev1])

y_dev = pd.concat([y_dev0, y_dev1])

X_test = pd.concat([X_test0, X_test1])

y_test = pd.concat([y_test0, y_test1])

# anomaly metric calculation

def metric(X, sig_cut, nfeatures):

# X: squared Z-score

y_metric = (X.sum(axis=1)/nfeatures)**0.5

y_pred = y_metric.apply(lambda x: 1 if x>sig_cut else 0)

return y_pred

# score calculation

def score(y_pred, y_actual):

def verdict(p,a):

# predict, actual

# True/False Positive/Negative

x=''

if p==0 and a==0:

x='TN'

elif p==0 and a==1:

x='FN'

elif p==1 and a==0:

x='FP'

elif p==1 and a==1:

x='TP'

else:

x='Invalid'

return x

y_score = pd.DataFrame({'predict':y_pred, 'actual':y_actual})

y_score['verdict'] = y_score.apply(lambda x: verdict(x['predict'],x['actual']), axis=1)

tp = y_score[y_score.verdict=='TP'].verdict.count()

tn = y_score[y_score.verdict=='TN'].verdict.count()

fp = y_score[y_score.verdict=='FP'].verdict.count()

fn = y_score[y_score.verdict=='FN'].verdict.count()

inv = y_score[y_score.verdict=='Invalid'].verdict.count()

if inv>0 :

print('Invalid value. Check classification values are all 0 or 1')

return 0

# Evaluation scores

precision = tp/(tp+fp)

recall = tp/(tp+fn)

f1score = 2*precision*recall/(precision+recall)

#print('TP = {}, TN = {}, FP = {}, FN = {}'.format(tp,tn,fp,fn))

return y_score.predict, precision, recall, f1score

Tune hyper parameters

df_hp = pd.DataFrame(columns=['sig_cut','nfeatures','lead_feature','precision','recall','f1score'])

df_y = y_dev.rename('actual').to_frame()

# This part is very slow

for icut in range(1,11):

sig_cut=0.5*icut

print(sig_cut)

# Train to sort leading features in order of "classification power"

dfz = (X_train1 > sig_cut).mean().sort_values(ascending=False)

sorted_feature = dfz.index.tolist()

for nfeatures in range(1,31):

lead_feature = sorted_feature[:nfeatures]

y_pred = metric(X_dev[lead_feature], sig_cut, nfeatures)

result = score(y_pred, y_dev)

y, p, r, f = result

new_name='predict'+str(icut)+'_'+str(nfeatures)

#print(new_name)

y = y.rename(new_name).to_frame()#

df_y = pd.merge(df_y, y,left_index=True,right_index=True)

df_hp = df_hp.append({'sig_cut':sig_cut,'nfeatures':nfeatures,'lead_feature':lead_feature,

'precision':p,'recall':r,'f1score':f}, ignore_index=True)

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

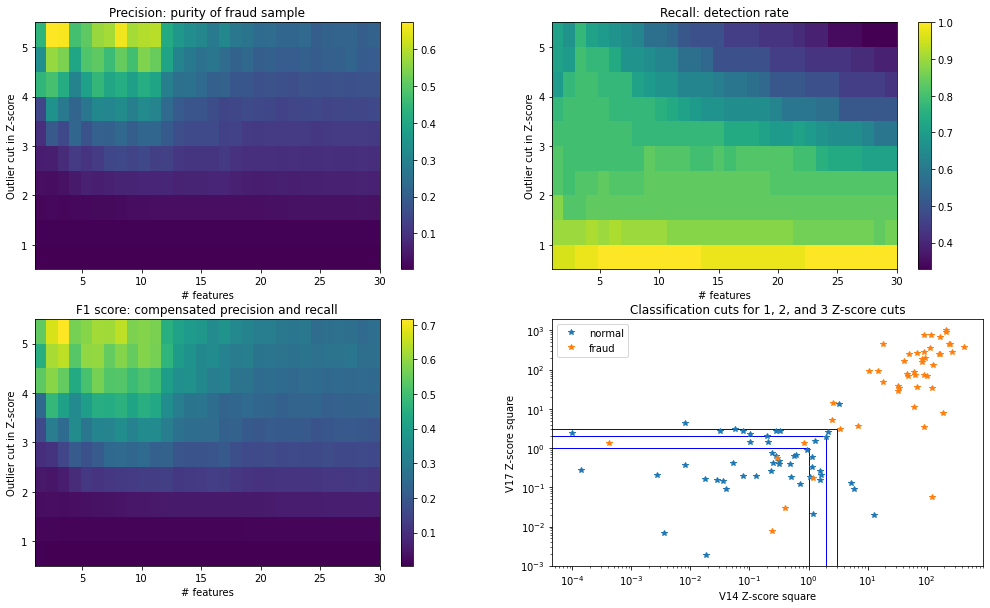

Visualize tuning result

fig = plt.figure(figsize=(17,10))

ax0 = plt.subplot(2, 2, 1)

plt.hist2d(df_hp.nfeatures, df_hp.sig_cut, weights=df_hp.precision, bins=[30,10], range=[[1,30],[0.5,5.5]])

plt.colorbar()

ax0.set_title('Precision: purity of fraud sample')

ax0.set_xlabel('# features')

ax0.set_ylabel('Outlier cut in Z-score')

ax1 = plt.subplot(2, 2, 2)

plt.hist2d(df_hp.nfeatures, df_hp.sig_cut, weights=df_hp.recall, bins=[30,10], range=[[1,30],[0.5,5.5]])

plt.colorbar()

ax1.set_title('Recall: detection rate')

ax1.set_xlabel('# features')

ax1.set_ylabel('Outlier cut in Z-score')

ax2 = plt.subplot(2, 2, 3)

plt.hist2d(df_hp.nfeatures, df_hp.sig_cut, weights=df_hp.f1score, bins=[30,10], range=[[1,30],[0.5,5.5]])

plt.colorbar()

ax2.set_title('F1 score: compensated precision and recall')

ax2.set_xlabel('# features')

ax2.set_ylabel('Outlier cut in Z-score')

n_fraud = len(X_dev1)

print(n_fraud,"fraud samples")

#print('leading features: ',df_hp[(df_hp.sig_cut==2)&(df_hp.nfeatures==30)].iloc[0].lead_feature[:2])

x0=X_dev0.sample(n=n_fraud).V14

y0=X_dev0.sample(n=n_fraud).V17

x1=X_dev1.V14

y1=X_dev1.V17

ax = plt.subplot(2, 2, 4)

plt.plot(x0,y0,'*')

plt.plot(x1,y1,'*')

c1 = plt.Rectangle((0, 0), 1, 1, color='b', fill=False)

c2 = plt.Rectangle((0, 0), 2, 2, color='b', fill=False)

c3 = plt.Rectangle((0, 0), 3, 3, color='b', fill=False)

ax.add_patch(c1)

ax.add_patch(c2)

ax.add_patch(c3)

plt.legend(['normal','fraud'])

ax.set_title('Classification cuts for 1, 2, and 3 Z-score cuts')

ax.set_yscale('log')

ax.set_xscale('log')

ax.set_xlabel('V14 Z-score square')

ax.set_ylabel('V17 Z-score square')

plt.show()

49 fraud samples

Interpretation of cross validation scores

Precision goes higher as the number of leading features increases until it reaches about 10, then decreases

- The more relevant features we use, the detection becomes more strict.

- When we start to use more irrelevant features, then the detection doesn’t enhance fraud selection.

Precision goes higher as Z-score cut increases

- Assuming normal samples have sharper distribution, higher z-score cut always increases purity of fraud sample.

Even at the highest, the precision is much lower than 1, due to heavily skewed statistics of classification samples

Recall goes higher as Z-score cut decreases

- Not all fraud samples are separable from normal samples, so lower Z-score cut will only keep more fraud sample.

- However the precision is very small in the lowest Z-score area.

Recall goes higher as the number of leading features decreases, except using only one feature

- For a given Z-score cut, using a few multiple leading features detect more fraud samples than using too many features.

The highest F1 score is achieved when 2-3 features with highest Z-score cut are applied

- Observation from precision and recall explain this result

- 2-3 leading features do best on ROC curve in the below, too

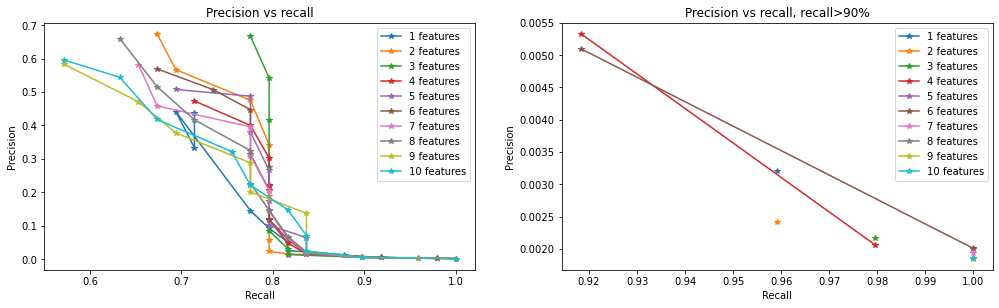

fig = plt.figure(figsize=(17,10))

ax3 = plt.subplot(2, 2, 1)

lgd=[]

for i in range(1,11):

plt.plot(df_hp[df_hp.nfeatures==i].recall, df_hp[df_hp.nfeatures==i].precision,'*-')

lgd.append(str(i)+' features')

plt.legend(lgd)

ax3.set_title('Precision vs recall')

ax3.set_xlabel('Recall')

ax3.set_ylabel('Precision')

ax3 = plt.subplot(2, 2, 2)

lgd=[]

for i in range(1,11):

plt.plot(df_hp[(df_hp.recall>0.9)&(df_hp.nfeatures==i)].recall,

df_hp[(df_hp.recall>0.9)&(df_hp.nfeatures==i)].precision,'*-')

lgd.append(str(i)+' features')

plt.legend(lgd)

ax3.set_title('Precision vs recall, recall>90%')

ax3.set_xlabel('Recall')

ax3.set_ylabel('Precision')

plt.show()

print(df_hp[(df_hp.recall>0.9)&(df_hp.nfeatures<11)]

[['sig_cut','nfeatures','recall','precision']].sort_values(by=['recall'],ascending=False).head(10))

print(df_hp[(df_hp.recall>0.9)&(df_hp.nfeatures<11)]

[['sig_cut','nfeatures','recall','precision']].sort_values(by=['precision'],ascending=False).head(10))

print(df_hp[(df_hp.nfeatures<11)]

[['sig_cut','nfeatures','recall','precision']].sort_values(by=['precision'],ascending=False).head(10))

print(df_hp[(df_hp.nfeatures<11)]

[['sig_cut','nfeatures','recall','precision']].sort_values(by=['recall'],ascending=False).head(10))

print(df_hp[['sig_cut','nfeatures','recall','precision','f1score']].sort_values(by=['f1score'],ascending=False).head(10))

sig_cut nfeatures recall precision

4 0.5 5 1.000000 0.001996

5 0.5 6 1.000000 0.002009

6 0.5 7 1.000000 0.001932

7 0.5 8 1.000000 0.001857

8 0.5 9 1.000000 0.001850

9 0.5 10 1.000000 0.001858

2 0.5 3 0.979592 0.002166

3 0.5 4 0.979592 0.002061

0 0.5 1 0.959184 0.003211

1 0.5 2 0.959184 0.002412

sig_cut nfeatures recall precision

33 1.0 4 0.918367 0.005327

35 1.0 6 0.918367 0.005096

0 0.5 1 0.959184 0.003211

1 0.5 2 0.959184 0.002412

2 0.5 3 0.979592 0.002166

3 0.5 4 0.979592 0.002061

5 0.5 6 1.000000 0.002009

4 0.5 5 1.000000 0.001996

6 0.5 7 1.000000 0.001932

9 0.5 10 1.000000 0.001858

sig_cut nfeatures recall precision

271 5.0 2 0.673469 0.673469

272 5.0 3 0.775510 0.666667

277 5.0 8 0.632653 0.659574

279 5.0 10 0.571429 0.595745

278 5.0 9 0.571429 0.583333

276 5.0 7 0.653061 0.581818

275 5.0 6 0.673469 0.568966

241 4.5 2 0.693878 0.566667

249 4.5 10 0.632653 0.543860

242 4.5 3 0.795918 0.541667

sig_cut nfeatures recall precision

4 0.5 5 1.000000 0.001996

5 0.5 6 1.000000 0.002009

6 0.5 7 1.000000 0.001932

7 0.5 8 1.000000 0.001857

8 0.5 9 1.000000 0.001850

9 0.5 10 1.000000 0.001858

2 0.5 3 0.979592 0.002166

3 0.5 4 0.979592 0.002061

0 0.5 1 0.959184 0.003211

1 0.5 2 0.959184 0.002412

sig_cut nfeatures recall precision f1score

272 5.0 3 0.775510 0.666667 0.716981

271 5.0 2 0.673469 0.673469 0.673469

277 5.0 8 0.632653 0.659574 0.645833

242 4.5 3 0.795918 0.541667 0.644628

241 4.5 2 0.693878 0.566667 0.623853

275 5.0 6 0.673469 0.568966 0.616822

276 5.0 7 0.653061 0.581818 0.615385

245 4.5 6 0.734694 0.507042 0.600000

244 4.5 5 0.775510 0.487179 0.598425

211 4.0 2 0.775510 0.475000 0.589147

How to select final parameters

Highest F1 (or F_{\beta}) score is often the best selection. From data, the highest F1 scores are archived by 2-3 leading features with highest Z-score cut. With such selection, the cross validation set shower good performances both in precision (40-60%) and recall (70-90%).

However, fraudulent transactions are so fatal, so you also want to keep a certain high recall value even though you lose some precision.

I selected final parameters based on the overall trends, not relying on precise scoring too much. Here are reasons.

-

The number of fraud sample has 10% of high statistical error assuming that it follows common probability distributions. Besides, this kind of anomaly sample distributions are chaotic.

-

I can imagine that the precision won’t be stable for each sampling or over time simply because the frequency of fraudulent transactions won’t be regular (if so, it will be interesting…). Here, note that recall might be relatively stable than precision, assuming fraudulent transactions have much broader distribution than normal one, until fraudulent transaction techniques are evolved and become close to normal transactions

As a conclusion, I suggest two parameter choices with two different kind of “best-overall” performance

Choice 1 - Highest precision at recall > ~90%

From cross validation set, top highest precision having recall > 90% were mostly achieved by parameters with a few multiple leading features (2-5 features) and moderately low Z-score cut (1.5-2.5) achieved.

Test

# Test

lead_feature = df_hp[(df_hp.sig_cut==2)&(df_hp.nfeatures==30)].iloc[0].lead_feature[:2]

y_pred = metric(X_test[lead_feature], 2, 2)

y, p, r, f = score(y_pred, y_test)

print(len(X_test), y.sum(), p,r)

print('precision:',p,'recall:',r,'sampling fraction:',y.sum()/len(X_test))

28531 1590 0.028930817610062894 0.92

precision: 0.028930817610062894 recall: 0.92 sampling fraction: 0.05572885633170937

From final test, 88% recall and 3.6% precision (number varies for different samplings) is obtained with 2 leading features and Z-score = 2 cut.

Evaluation

-

System with ~90% recall means that this system catches 90% of fraudulent transaction, which sounds very safe.

-

From our model, the precision was a few percent, which is too low to halt (customers will be annoyed), however, quite high to be the first level of sampling.

-

The advantage of this sampling is that it reduces the size of “samples to be investigated” significantly without losing most of fraudulent samples, therefore, we can build a several levels of efficient detector.

Application

-

One application example can be building multiple levels of fraud detector, combining faster first level and slower second (or higher) level

-

Level 1: Implement this model in as a fast hardware process, for example, add an operation which processes signals of two features and makes logic operation for comparison and decision in a card reader chip. If level1 detect fraud-like transaction, then it halt transaction and send feature signals to level 2

-

Level 2: Perform further and slower classification using software or information of higher-up security levels. If this decision says normal, then the transaction will be made (with delays introduced by level 2 processing time), and a customer will hardly notice anything. If this decision says fraud, then we can contact customer to ask security information.

Choice 2 - Highest F1 score

Highest F1 scores are achieved by parameters of 2-3 leading features and highest Z-score cut. From cross validation set, such parameters show good performance for both precision (40-60%) and recall (70-90%).

Test

lead_feature = df_hp[(df_hp.sig_cut==5)&(df_hp.nfeatures==30)].iloc[0].lead_feature[:3]

y_pred = metric(X_test[lead_feature], 5, 3)

y, p, r, f = score(y_pred, y_test)

print('accuracy:',y,'precision:',p,'recall:',r,'f1score:',f)

accuracy: 109266 0

29673 0

51913 0

61682 0

117402 0

..

153 1

188 1

61 1

40 1

169 1

Name: predict, Length: 28531, dtype: int64 precision: 0.6607142857142857 recall: 0.74 f1score: 0.6981132075471698

From final test, 77% recall and 74% precision (number varies for different samplings) is obtained with 3 leading features and Z-score = 5 cut.

Evaluation

- This system samples highly fraud-like transactions without losing too much of total fraud transactions. Considering only 0.17% are fraud, 74% of test precision is such a great focusing on crime.

Application

- One application can be a fast hardware level implementation in a card reader. If a transaction is marked as fraudulent, then the transaction is automatically halt, the transaction information is sent to security monitoring places and/or a staff in a shop can ask further questions to the credit card user.

Discussion and Conclusion

-

Supervised anomaly detection model based on Z-score is built for fraud detection.

-

Two best models are suggested, both perform excellent on test set

-

As the trend of normal or fraud transaction changes, the parameters should be adjusted. This model provides intuitive way to tune the parameters.

-

Some features might have skewed distribution. In such case, transformation to log might work better.

-

Of course, knowing the meaning of each feature will significantly improve the model.

Leave a comment